How does UK retirement income compare with the rest of the world?

Thursday 11 January, 2018

Thomas Oliver’s Financial Adviser and Financial Planner, Tracy Dove reviews how much UK retirement income our pensioners receive compared with those in other countries.

She also considers the new pension freedom and choice options by comparing the advantages of annuities and flexible access drawdown.

Do we have the correct infrastructure, social awareness and knowledge to understand how much retirement income we require to achieve our financial goals in retirement?

I will be addressing this question and comparing the UK with other countries to see what areas of retirement planning we do well, and where we could improve our pension planning.

When comparing UK retirement income to other developed nations it appears that during the transition into retirement our population suffers from a much larger fall in real income compared with other developed countries. Various think tanks have recommended that the UK add various measures to prevent any crisis and ensure future retirees do not lose out.

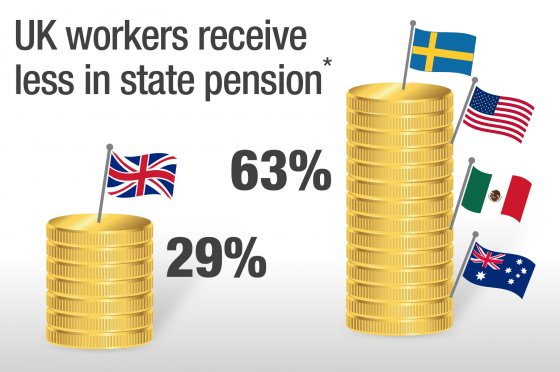

OECD report shows that British workers receive less in state pension than many other developed countries when they retire

The Organisation for Economic Co-operation and Development (OECD), an inter-governmental economic organisation revealed that British pensioners receive only 29% of the average working wage from state schemes once they retire. 63% is the typical proportion received in other member states. This includes Mexico, Latvia, and Korea, the USA, Australia, New Zealand and Nordic countries.

The report promoted the importance of maintaining incentives to encourage people to save and make sure they have confidence that governments will support them in saving for their retirement. However, it is obvious that some countries have better state pension provision, while others including the UK encourage individuals to supplement this state income with private pension policies.

OECD recommends UK population offer better incentives to save for retirement

The OECD concluded that the UK population must be offered better incentives to save more for their retirement. Private pensions are well placed to fill the gap in terms of retirement income and workplace pensions are a positive development. As Tracy Dove, pension adviser London mentioned in a previous article: Are you saving enough for your retirement? more private savings schemes must be offered so the working population are encouraged to consider their retirement planning and save for the long-term, this however has a cost to the government.

Tracy Dove, Financial Adviser and Retirement Planner in Essex and London said: ‘The Pension Freedom laws which have been changed recently have had a positive impact on how people view saving for the long-term. Many clients now understand how retirement planning can benefit them and their families too. Before these new rules came into effect most people would simply buy an annuity, which gives an income for life for the individual.’

How does a pension annuity work?

For example: if you give £100,000 to a life and pensions provider and you meet their criteria at current interest rates they will pay you an income of approximately £5,000 GBP per year for the rest of your life. Please note this is the current level paid out due to historic low interest rates.

The downside to the pension annuity is if you die shortly after receiving the annuity the policy will die with you and your family are not entitled to any income from it. This was always historically a disadvantage of purchasing an annuity for your retirement.

How can flexible access drawdown assist with retirement planning?

Now you have the option of flexible access drawdown so you take the pension income you need each year. If you work with a financial adviser you can make your capital work for you without depleting the capital by taking any growth achieved each year. In the event you pass away with the correct financial planning in place you can now pass this asset to your family, in some cases tax free.

Tracy Dove, Pension Adviser and Retirement Planner in Essex and North London continued: ‘Although the new pension freedoms are a positive improvement for retirement planning, in the UK there still appears to be a lack of understanding about the best way to save for the future, so some clients we see do not have adequate pension provision. Some people think they cannot afford to save for the future now so do not save into a pension. This view is extremely worrying for our future retirees. I recommend that anyone reviewing their retirement planning takes advice from a financial adviser who can set up a realistic savings plan and give some examples of how much money you will receive in retirement based on your current savings and any expected state pension.

Everyone has different needs and requirements in retirement and it is important that you regularly review your own financial goals and requirements. Often our clients find their household spending is higher in the first few years after they stop work and they budget for lower spending in later years. A financial adviser can also explain the new pension freedom and choice options to you. They do improve your pension choices but we recommend our clients undertake pension planning so they understand how the new pension options work and they do not withdraw too much income with the flexible access drawdown option.

At Thomas Oliver we offer a free initial financial planning consultation. If you would like to arrange a meeting with a qualified financial adviser please contact me on 01707 872000.’